2026 Tax Outlook

KEY HIGHLIGHTS

Updated Tax Brackets

Increased Standard Deduction

Expanded Opportunities for Planning and Maximization of Tax Efficiency

With 2026 off to a volatile start, there are many “what if?” moments confronting individuals. While legislative differences are at the forefront of our world today, taxes are inevitable no matter the controlling party. While taxes are, for the most part, unavoidable, a strategic plan can assist in minimizing the overall tax burden.

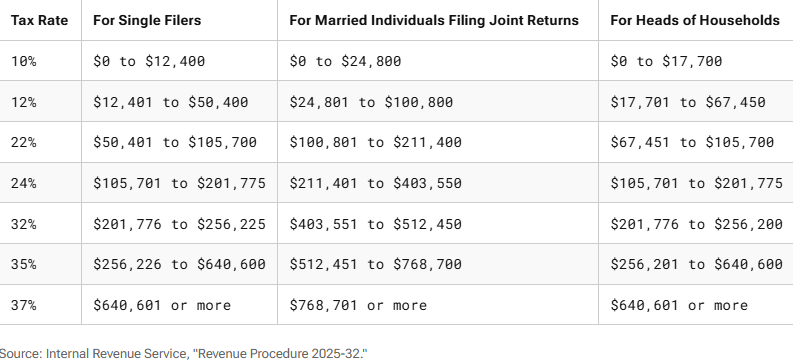

1. UPDATED TAX BRACKETS

Adjusted for inflation, the IRS has updated the 2026 income brackets to reflect the applicable federal tax rate.

2. FOCUS ON SAVING INCENTIVES

If you have not already contributed to an IRA or HSA for 2025, you have until April 15, 2026 to do so. If you are a resident of a state with a federal disaster designation for 2025 or are a victim of California’s Palisades fires, you may have additional time to file your tax returns and make tax payments. 529 College Savings Accounts are a great way to plan for your child’s future. Whether you are a new parent or have multiple or are a generous grandparent, a 529 savings account can assist with the rising costs of education.

For tax year 2026, you can contribute up to $7,500 - that’s a $500 increase from 2025. One thing to remember is deductions for IRA contributions operate on a phase-out schedule. Meaning, depending on your level of income for the given year, you may be eligible to a deduction (i.e. reduce your overall MAGI) for allocating funds to your IRA. It is important to note that traditional IRA and Roth IRA contributions are determined on an aggregate basis. That means you cannot exceed the $7,500 contribution limit across both accounts.

Consult a tax professional for more ways to take advantage of the many offered incentives.

3. CONSIDER CONVERTING TO A ROTH

Many individuals find themselves in pre-tax accounts (e.g. traditional 401k or traditional IRA). While this may be an ideal plan for some, does not mean it is a one-size fits all. Converting to a Roth entails contributing after-tax funds to the specific account. Once the funds are in the account, the funds will grow tax-deferred. Upon the attaining the age of 59 1/2, the distributions from the Roth account could be tax-free and penalty-free. There are various exemptions made available in the applicable Internal Revenue Code sections, consult an advisor for additional insight.

TAKEAWAY

Tax planning is not completed overnight and almost always requires consistent planning throughout the year. If you want to reduce your overall tax liability or plan for the long-haul, implementing a tax-efficient investing plan that works for you is a non-starter.